2020 Austwine Market Update

Has Time Warped?

It is hard to believe that so little real time has elapsed since the first cases of COVID-19 appeared late in 2019. Since then, time seems to have warped as a result of the pandemic: days have seemed like weeks, and weeks have seemed like months. All of us have struggled to understand what this invisible enemy means for our livelihoods and, even more importantly, our lives. This short article examines some of the issues facing the bulk wine business in Australia that have arisen during the course of the pandemic.

Constrained Supply: Drought, Fires & Very High Water Prices

This past summer seems like ancient history, but for many Australian wine producers the impacts of an extremely difficult vintage remain very real. The fires impacted so many regions in Australia with countless wineries and growers affected in regions such as the Adelaide Hills, Kangaroo Island, North East Victoria and the Hunter Valley. It has been heartbreaking to see and hear about the destruction caused by the fires and, in some cases, whole vintages have been lost.

Furthermore, the impact that the subsequent COVID-19 shutdowns have had on these businesses has been a massive second blow. Their plight arising from bushfire devastation seems to have been forgotten in the shadow of the widespread economic devastation brought about by COVID-19. So complete was the local economic shutdown that a kangaroo was seen hopping through Adelaide’s deserted city streets during April.

Even without the fires crop levels were extremely low, particularly for Premium Regional wines, to levels not seen since the 2007 drought.

Low water allocations and resultant high water prices, also not seen since 2007, have severely impacted many Inland Commercial wineries and grape growers. Even those with permanent water entitlements were forced to buy temporary water, as low allocations in Victoria persisted throughout this past summer.

Chardonnay, which has a lower revenue per hectare than the major red varieties, was typically rationed for water and so modest tonnes were harvested. Other white varieties with low revenue per hectare, such as Semillon and Colombard, shared a similar fate.

Bulk Wine Listings: Down Then Up, Now Down Again

As vintage approached, we saw many wineries withdraw their bulk wine listings as their estimates of 2020 vintage tonnages shrank.

A short vintage, arising from consecutive drought years, was expected to cut a swathe through 2020 vintage wine grape production. For example, Clare Valley, Barossa and McLaren Vale all expected, and indeed all experienced, extremely short crops.

We then witnessed a period of increased bulk wine listings as wineries grappled with the impact of COVID-19 on their sales.

Every winery was different and much depended on their mix of business through various sales channels.

As a very crude generalisation, the impact of the pandemic on different sales channels looked like this:

- Cellar door Severely reduced; on Government funded life support.

- On-premise Severely reduced; on Government funded life support.

- Off-premise Brisk during the initial outbreak; perhaps now has peaked.

- On-line/direct Brisk during the initial outbreak; perhaps now has peaked.

From about mid-March, as COVID-19 shutdowns began in Australia, forecasting likely sales levels became almost impossible for many wineries.

An avalanche of news flows made assumptions about likely demand profiles obsolete. Forecasts were thrown out the window due to the pandemic, and every winery’s exposure to the above sales channels was, and remains, different. Since the shutdowns began, wineries have become somewhat accustomed to living with extremely low forecasting visibility, but the key questions wineries are grappling with seem to be:

- Is our bulk wine inventory now in surplus, or shortage, or balanced, when compared with expected sales?

- Did the short 2020 crop mean we are actually short of bulk wine, or has the pandemic changed that?

- What will be the rate of sales recovery as shutdowns and restrictions are eased?

- What happens if there is a widespread second wave of infections?

What we can say, is that the volumes available on our current bulk wine availability is extremely low indeed.

Extreme Pricing Volatility

Pricing volatility has prevailed as a result of all the uncertainty on both the supply side (lower 2020 wine grape crops) and the demand side (COVID-19).

In other words, the pricing differentials amongst willing sellers has enlarged greatly. So have the pricing differentials amongst willing buyers.

This has been especially pronounced for Premium Regional wines. Whilst it is certainly usual to have differences in transaction prices in this part of the market, the difference since COVID-19 has been significant.

Inland Commercial wines are experiencing less pricing volatility.

Bulk Domestic Wine Sales

This market awoke earlier than usual from its traditional vintage slumber with demand from the fire ravaged regions such as the Adelaide Hills.

Buyers spilled onto the market to try and cover their requirements, creating opportunities for those who suddenly found themselves with surplus stocks arising out of the pandemic.

Demand in this market has been steady, but buyers are very constrained and very cautious due to the pandemic. Planning horizons have shrunk dramatically.

The mantra in the market place has been: let’s just solve today’s problem today, tomorrow’s problem tomorrow, and forget about trying to solve next month’s problems. Next year is an age away.

Bulk Export Wine Sales – “The Big Shift”

In contrast to the steady, cautious demand in the domestic market, export inquiries have been coming thick and fast from most markets, except, most notably, China.

Those in the wine business lucky enough to still be in business and keep their jobs have put in some big hours trying to keep on top of a rapidly changing environment.

As jobs and revenue disappeared from hotels and restaurants, short term pantry filling drove sales through supermarket and on line channels, as consumers responded to frightening daily media briefs from their political leaders.

Most markets that we export to have gone through this broadly similar pattern of a big shift in sales away from on-premise to off-premise sales, although the timing has been staggered according to local lock down protocols.

Buyers operating in on-premise channels have asked for contracts to re-written, forgiven, or changed. Payment extensions have been requested. Forecasts have been slashed. Many requirements from vintage 2020 are still unknown.

In contrast, buyers operating in off-premise and on-line channels have more than taken up the supply that would otherwise be going to on-premise consumption. However, these changes are very uneven, across different markets, messy and requiring a lot of ongoing care and attention to properly meet buyers’ needs. This has resulted in an explosion of workloads for the suppliers of these channels.

Impacts of Large Northern Hemisphere Inventories

Large inventories and crops in the Northern Hemisphere will add another level of complexity to the calculations of Australian wine producers as they navigate export markets.

Australia could experience its lowest wine grape crop since 2007 and, despite modest 2020 crops in Chile and Argentina, Australia is likely to lose market share as listings move to more competitive supply sources.

The high price of both temporary water and Inland Commercial grapes in Australia has crimped Australia’s competitiveness this year in comparison to other supplying nations.

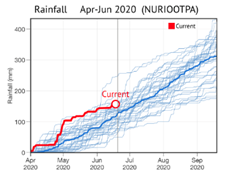

Rainfall Outlook Much Improved

All of this could change during this winter, as many regions of Southern Australia have experienced the best autumn rains in years.

Opposite is the last 3 months rainfall at Nuriootpa (Barossa) illustrating the good early rains since May 2020.

It is too early to call the end of the current Australian drought, but at around Easter time, the Darling River met the Murray River for the first time in 2 years. A great sign of replenished water sources.

Water in Murray Darling Basin storages has increased from a seasonal low of 31% late in summer, to 40% during this past week. This is 14% points more than the same time last year, with still many months of wet conditions likely to come.

Temporary water prices have also fallen from their summer peak of near $1,000 per megalitre to around $200 per megalitre, closer to the long term average.

The rainfall outlook for August – October shows wetter months ahead with above average rainfall expected for many areas of Eastern Australia.

All this is good news for more favourable growing conditions ahead of the 2021 vintage, although in the current environment, the next year’s harvest feels like a decade away.

Conclusion – Our Actions Now Will Be Remembered

It is extremely difficult to draw any reasonable conclusions from this mish-mash of circumstances that we find ourselves in. Our environment is changing too fast and the data points are too unfamiliar, too conflicting and often with untested veracity. Is trying to make sense of it all just a fool’s errand?

Instead, should we rely on a more simple strategy: reach out to your customers, your suppliers and your employees to constructively resolve the problems and opportunities thrown up by the pandemic.

Your trust in these people and the relationships built in better times are critical right now as all humanity shares a similar fate in the face of COVID-19. With a little luck, help and cooperation from our business partners and friends we will maximise our industry’s chances to survive and prosper.

Actions taken during a crisis will echo down the years: now is the time to help one another through this pandemic.

Sign up

Sign up to receive the latest news and offers from Austwine.